In the first of our occasional Meet the Manager interviews, we spoke to Richard Philbin, Chief Investment Officer at Wellian Investment Solutions about Brexit and the impact of the Leave vote.

Following the US election result earlier this month, we thought it would be an excellent opportunity to ask the experts at LGT Vestra what they think are the threats to be aware of and the opportunities to be grasped.

Although this absolutely does not constitute a recommendation to invest in LGT Vestra (we are of course, independent and have relationships with a wide selection of firms), we thought you might like to hear their views following the vote and how they have positioned their portfolios now and into what it looks like may be, a turbulent 2017.

So we asked Phoebe Stone (PS), Model Portfolio Manager at the firm, a number of questions:

CG – How did your team position the LGT Vestra portfolios in the run up to the election and did you forecast a Trump win?

PS – The work that was done by the LGT Vestra equity research department concluded that a Trump win was very much possible. However, we didn’t expect the support for Trump to be as strong as it turned out to be. Because of the lack of clarity and detail in Trump’s policies throughout the campaign trail, it was difficult to get a good understanding of the impact that his election as President would have on global economies and nations.

In terms of positioning, gold exposure was added to portfolios. This was to act as our ‘insurance policy’ in case Trump was elected and the markets fell in response. This worked initially but since then gold has sold off in line with increasing implied US real interest rates and a surging dollar as investors have u-turned on Trump.

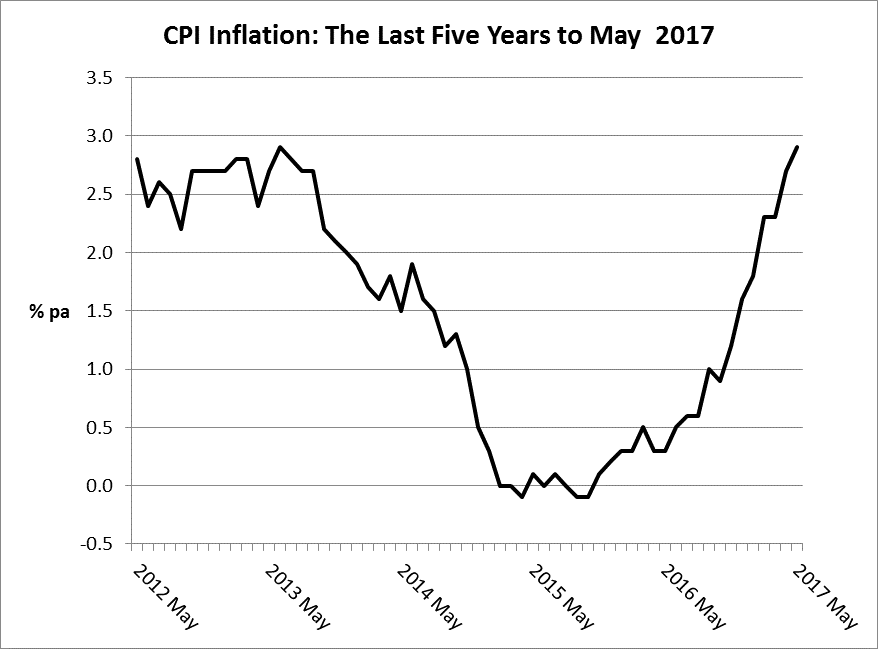

Gold remains an important asset in portfolio construction particularly at a time in which we could see persistent inflationary pressures as a result of fiscal stimulus by governments. In this type of environment, holding an allocation to gold is a prudent hedge.

CG – How are your investment managers taking advantage of the new uncertainty?

PS – The most remarkable thing we have seen since the Trump election is how quickly the markets have shifted. From initial falls in equity markets stemming from uncertainty over what an elected Trump would result in, the markets have undergone a massive rotation.

We saw investors in the days following the election fleeing bond markets as they expected the President-elect’s stimulus policies to generate strong US GDP growth and consequent inflation. In this scenario bonds are relatively less attractive than equities. With bond prices falling and corresponding yields rising, investors looking to achieve specific levels of income could start to view the fixed income arena as more attractive, without the equity risk of dividend income.

CG – In light of the vote for Trump, do you foresee any immediate portfolio changes?

PS – We are certainly in for a rockier ride than if Clinton had been voted in. In terms of portfolio positioning, we have been reducing our sovereign debt exposure over the past few months ahead of the US election. We were therefore sheltered from the falls in the bond market seen during November. This was triggered by the rotation out of bonds and into equity on the Trump rally. Following the election of Trump we increased our exposure to both US mid-cap equities and global value equities in the higher risk portfolios. Trump’s protectionist and US-centric policies are likely to most benefit US small-cap companies and cyclical stocks (held in global value strategies), as investors anticipate stronger GDP US growth ahead.

CG – What might the long term effects of a Trump Presidency be? Will this be positive or negative for investors?

PS – A lot of attention since President-elect Trump’s victory has been on fixed income markets. We have seen a consequent selloff in bonds across the globe. Many people have been predicting a reversal for bond markets after years of falling interest rates. Could this be the start of a much bigger move or a short term correction? Bond markets are driven by interest rate expectations and supply and demand. With many central banks targeting inflation, the path of interest rates is dependent on long-term inflation expectations.

Globalisation has kept prices low as manufacturing was able to move to the cheapest parts of the world. Trump’s indicated trade policy would be a retreat from this and would involve raising tariffs on imports. If the UK fails to make a good post-Brexit deal on trade with Europe, a similar effect will be felt here. These are potentially one-off effects but do remain a concern.

Another concern for markets is the influence on prices, supply and demand. Donald Trump, in his acceptance speech, only mentioned one real policy and that was to increase infrastructure spending, which would imply more government borrowing. Interestingly, at the Conservative party conference there was also talk of a relaxation of the previous Chancellor’s austerity measures, which could mean more supply in the Gilt market.

As for Trump, we will see how much US Congress will let him do in the months to come. In many ways there are still deflationary forces at work. Globalisation cannot be entirely reversed and internet price checks, automated production and an ageing population all mean that we are probably not in for a long-term higher inflation rate. Given the amount of gearing in the global economy, in both government and private sectors, any rise in interest rates will be a further constraint. Thus we believe that official rates will only rise very slowly in the UK and US despite short-term inflation threats. However bond markets may remain volatile as fears come and go.

CG – Given the protectionist rhetoric we heard throughout Trump’s campaign, what do you think the biggest challenge will be for our clients over the next 4 years?

PS – Trump’s election is another catalyst for the increased levels of volatility that we have been experiencing in markets since last August. Initially triggered at that time by concerns over China’s GDP growth rate, and followed by the fall in the oil price there has been increased volatility in equity markets driven by macroeconomic events. Interest rate cycles and political events (Brexit, US Presidential Election) have all contributed. One thing that unites these events is the consequent uncertainty; we don’t know at this point how each will pan out, what the effects will be on the economy, society and on each other.

We believe the volatility we have seen permeating markets is here to stay, and this will therefore be the biggest challenge for clients. In portfolios we are specifically focused on managing the volatility, using absolute return funds for example, to provide ballast to the ship. This will smooth the path of return during a time when macroeconomic events continue to shake markets.

CG – Looking forward to the European political scene, a number of countries in Europe have important elections coming up in 2017. What are LGT Vestra’s views on the political climate in Europe and how are you positioning your portfolios to take advantage of potential changes.

PS – After President-elect Trump’s success and following the ‘Brexit’ referendum over the summer, potential constitutional crises have never been more in vogue. With this in mind, the world’s attention will now shift to the upcoming referendum in Italy. On 4th December, the Italian electorate will go to the polls to vote on the fundamental changes to their country’s constitution. The referendum is also another opportunity for the populists, buoyed by results from elsewhere in the world, to land another blow against the established mainstream. In Italy this is led by the ‘Five Star Movement’, notably led by a comedian (literally, rather than the accusation levelled at other similar parties) and is highly Eurosceptic.

Next year will bring a Dutch general election and French presidential election in spring, with German federal elections to follow later. Anti-Europeans are doing well and will only gain more momentum if the Italian referendum is interpreted as another vote against the establishment.

In terms of portfolio positioning, we have reduced our exposure to Europe in light of the upcoming uncertainty. We are also exposed to Europe on a hedged basis which will allow the portfolios to benefit from a falling Euro versus Sterling (likely with the uncertainty surrounding the future of the Eurozone).

CG – What are the key points for clients to be optimistic about?

PS – We continue to see value in equity markets, the asset class that will drive portfolio performance over the next four years. We are selective in terms of exposure, for example in the UK equity space, choosing to use active fund managers who are able to get access to areas of the market in which there is particular value. The election of Trump has acted at a catalyst of sea-change. Despite there being a multitude of uncertainties ahead, this change has already thrown up a huge amount of opportunities and from an investment perspective, will generate new drivers of growth and prospects.

As ever, we appreciate that each client is very different, with widely varying circumstances. This article is for informational purposes only. It is considered to be a general market commentary and does not constitute advice or a personal recommendation or take into account the particular investment objectives, financial situations or needs of individual clients. It is not intended and should not be construed as an offer, solicitation or recommendation to buy or sell any investments. You are of course recommended to seek advice concerning suitability of any investment from us.

Past performance is not a reliable indicator of future performance; and the value of investments, as well as the income from them can go down as well as up, and investors may get back less than the original amount invested.

The information and opinions expressed herein are based on current public information we believe to be reliable; but we do not represent that they are accurate or complete, and they should not be relied upon as such. Any information herein is given in good faith, but is subject to change without notice. No liability is accepted whatsoever by LGT Vestra or its employees and associated companies for any direct or consequential loss arising from this document.